3 min

05-May-2025

Managing the Medical Equipment Loan Payment Status is crucial for individuals and healthcare facilities relying on financed devices for patient care. Whether it's a wheelchair, ventilator, or advanced diagnostic machine, understanding the payment status helps ensure uninterrupted access and avoids late fees or service disruptions. This status includes key details like the remaining balance, due dates, past payments, interest rates, and any penalties or outstanding amounts. Staying updated allows borrowers to plan budgets, prevent defaults, and maintain good credit standings. Many lenders also offer online portals or mobile apps where users can conveniently track payments and receive alerts. For hospitals and clinics, monitoring payment status helps with cash flow and compliance reporting. Whether you’re a patient managing a home-use device or an administrator overseeing multiple equipment contracts, keeping track of your medical equipment loan status is essential for financial control and uninterrupted medical support. Always review your payment status regularly and act promptly.

Review loan documents

When you first receive your medical equipment, review the loan agreement thoroughly. The agreement will contain essential details such as the total loan amount, payment schedule, due dates, and interest rates. This document is a good starting point to understand your financial obligations.

Visit the lender’s website or portal

Many lenders provide online platforms or mobile apps where you can log in and view your loan status. Once logged in, you can check the current balance, upcoming due dates, and previous payments. Ensure that your login credentials are secure for privacy reasons.

Set up payment reminders

Most lenders offer email or text alerts to remind you of upcoming payments. Set up these reminders to avoid missing deadlines. You can also configure notifications for any overdue payments or important changes to your loan terms.

Call the lender’s customer service

If you don’t have access to an online portal, or if you prefer speaking to someone directly, call your lender’s customer service line. Ask them for a current breakdown of your loan payment status, including the remaining balance, next due date, and any potential fees or penalties.

Check your bank statements

Cross-check your bank account or credit card statements to verify that payments have been deducted correctly. Ensure that no payments are missed or processed incorrectly. If there’s any discrepancy, reach out to your lender immediately for clarification.

Request an account statement

If you prefer a more formal overview of your payment status, request a written statement from your lender. This will provide a detailed history of payments made, outstanding amounts, and interest accrued. It can be useful for budgeting and ensuring everything is up to date.

Monitor payment history

Keeping track of your payment history will help you identify any potential issues, such as accidental missed payments or delayed transactions. A good payment history may also improve your credit score, especially if you’re paying on time.

Consider setting up automatic payments

To avoid forgetting payments, consider setting up automatic payments directly through your bank or lender. This can ensure that payments are made on time without you having to worry about manually making each payment.

Review loan status regularly

Make it a habit to review your loan status regularly, even when you’re not due for a payment. Monitoring your loan ensures there are no surprises and gives you peace of mind knowing exactly where you stand financially.

By following these simple steps, you can easily manage your medical equipment loan and ensure that your payments are on track. Consistent tracking and communication with your lender can help avoid any financial hiccups down the road.

Avoid late fees and penalties

One of the most immediate benefits of tracking your loan payment status is preventing late fees and penalties. Missing a payment or paying late can result in additional charges, which can increase the overall cost of the loan. Regularly monitoring your payment status helps you stay on track and avoid unnecessary expenses.

Maintain good credit health

Timely payments play a significant role in maintaining or improving your credit score. Late or missed payments can negatively affect your credit rating, which could impact your ability to get approved for future loans or credit. By tracking your payments and ensuring they’re made on time, you safeguard your credit health.

Identify payment errors quickly

Regularly reviewing your loan payment status helps you spot discrepancies or errors in your account. For example, payments might be recorded incorrectly, or fees might be charged that shouldn’t be there. Early detection of such issues allows you to address them promptly with your lender.

Stay on top of loan terms

Loan agreements can have specific terms, such as fluctuating interest rates or the ability to make additional payments without penalties. By tracking your payment status, you stay informed about any changes in the loan's terms, such as updated due dates or interest rate adjustments. This helps you plan your budget accordingly and manage the loan more effectively.

Avoid service interruptions

When it comes to medical equipment, not paying on time can lead to interruptions in service, which could affect your ability to care for patients or manage your healthcare needs. By tracking your payment status, you ensure that payments are made on time and that your equipment continues to be available without disruption.

Budgeting and financial planning

Keeping track of your loan payment status allows you to factor your payments into your budget. By knowing how much is due and when, you can allocate funds accordingly, reducing the chances of financial strain. It helps you prioritise expenses and make adjustments if necessary to stay within your financial means.

Peace of mind

Regularly checking your loan status provides peace of mind. When you know your payments are up to date, and there are no surprises, you can focus on other aspects of life or work. Being proactive about your loan management reduces stress and provides confidence in your financial management.

Informed decision making

Tracking your payment status allows you to make informed decisions about refinancing, making extra payments, or exploring other options. If you’re ahead on payments, you may decide to pay off the loan faster, reducing the overall interest. Being aware of your loan status empowers you to take control of your financial future.

Improved financial relationships

Keeping up with loan payments strengthens your relationship with the lender. A consistent payment history reflects positively on you and may open up more favourable terms if you need future financial assistance. Lenders may be more inclined to offer discounts, better rates, or other benefits if you maintain a solid repayment record.

Incorrect loan balance displayed

Sometimes, the loan balance shown may be incorrect due to payment processing delays or data entry errors. This can happen if payments were made recently but haven’t been updated in the system yet.

Solution: Always check the date of the last payment and give it some time for the system to reflect changes. If the error persists, contact your lender for clarification and ask for an updated statement.

Technical issues with online portals

Online portals or mobile apps used to track your loan payment status may experience technical difficulties, such as login issues, slow loading times, or crashes.

Solution: Ensure that your internet connection is stable. If the problem is with the portal, try clearing your browser cache or updating the app. Contact customer support if the issue continues.

Delayed or missing payments

Sometimes, payments may be delayed or go missing in the system, making it appear as though you missed a payment. This can happen due to issues with bank transfers, processing errors, or misunderstandings about the payment method.

Solution: Double-check your bank statements or payment confirmation emails. If you find discrepancies, contact the lender to confirm whether the payment was received. Consider using automatic payments for smoother processing in the future.

Confusion over interest rates or fees

Some loan agreements may involve variable interest rates or additional fees that are hard to track. Confusion over how these are applied can make it difficult to understand your current payment status.

Solution: Review the loan agreement to understand how interest rates and fees are calculated. If there are any discrepancies, ask your lender for a breakdown of how your payments are being applied.

Difficulty navigating the loan management system

Some lenders use complicated or outdated systems for managing loans, which can make it difficult for borrowers to access accurate payment details quickly.

Solution: Reach out to customer support for guidance on how to navigate the system. You may also request that the lender provide statements via email or paper if the online system is difficult to use.

Disputes over payment dates

Loan agreements may include flexible payment dates, but confusion can arise about the exact due date. This is especially true when payments are made close to the end of the month or when the loan provider has set a specific day for payment each month.

Solution: Always verify your due dates and set calendar reminders ahead of time. If you miss a payment, ask for a grace period or clarification on due dates to avoid penalties.

Miscommunication or lack of updates

Sometimes, borrowers may not receive timely updates from their lenders, leaving them in the dark about the current status of their loan payments. This could lead to missed payments or misunderstandings about the loan’s progress.

Solution: Regularly check your account and ensure that the lender’s contact information is correct. Set up email or text alerts to receive updates on your payment status.

Unclear terms and conditions

In some cases, the terms and conditions related to your loan payments may not be clear, especially if the loan was taken out a long time ago. This can result in confusion about payment amounts, due dates, or loan details.

Solution: Review the loan agreement again or ask your lender for a detailed explanation of the terms. Understanding the specifics of your loan helps you avoid surprises down the line.

Security and privacy concerns

When checking your loan payment status online, there may be concerns about the security and privacy of your financial information. Data breaches or unsecured platforms can make it difficult to trust the loan management system.

Solution: Always ensure that the website or app you’re using is secure (look for HTTPS in the URL). Use strong, unique passwords, and enable two-factor authentication for additional protection.

Unforeseen changes in payment terms

In some cases, lenders may change the terms of the loan, such as interest rates or payment schedules, without clear communication. This can cause confusion about your payment status.

Solution: Read any communication from your lender thoroughly and immediately contact them if any changes are unclear. Ask for detailed explanations and request updated statements reflecting new terms.

Set up automatic payments

One of the easiest ways to ensure your loan payments are made on time is to set up automatic payments. Link your bank account to your loan account, and have payments automatically deducted each month. This eliminates the risk of forgetting a payment. Pro Tip: If you want to track your payments, use your lender’s platform to check loan details regularly.

Use payment reminders

Set reminders on your phone or through your lender’s app or website. Most financial institutions allow you to receive payment alerts via email or SMS a few days before your due date. This gives you a heads-up to ensure the funds are available in your account.

Tip: Utilise your lender’s notification settings for reminders about your upcoming payments.

Review your loan payment schedule

Understanding when your payments are due and how much is required can help you prepare in advance. Regularly reviewing your loan payment schedule will allow you to allocate the necessary funds before the due date. Pro Tip: You can easily check loan details to keep track of the payment schedule.

Link your loan to your calendar

Synchronise your loan due dates with your digital calendar. Set recurring events or reminders for a few days before the payment is due. This visual aid can help you see upcoming payments alongside other financial obligations, helping you prioritise accordingly.

Maintain a separate savings account for loan payments

Having a separate account specifically for loan payments can prevent you from accidentally spending the money you’ve set aside for your loan. Deposit the required amount into this account every month, ensuring the funds are available when needed.

Plan for extra payments

If your loan allows it, consider making additional payments on your loan when you have extra funds. This can reduce your balance and shorten the repayment period, but it also helps keep you ahead in case of unexpected events that might affect your finances.

Check your loan statement regularly

Regularly reviewing your loan statements will help you stay informed about your balance, interest rates, and upcoming payment amounts. This will give you enough time to plan for payments or adjust your budget accordingly. Tip: You can view your Bajaj EMI loan statement to see detailed information about your loan payments and history.

Ensure sufficient funds are available

Before the payment date, ensure that your account has sufficient funds to cover the loan payment. Insufficient funds can result in failed payments and possible fees. Keep track of your account balances to avoid this issue.

Review and adjust your budget

Make sure your loan payment is factored into your monthly budget. Track your spending habits and make adjustments as needed to prioritise loan repayments. This can help you avoid any financial strain when payment time comes.

Communicate with your lender in case of difficulty

If you’re facing financial hardship or foresee difficulty in making a payment on time, contact your lender immediately. Many lenders offer payment deferrals or flexible plans in case of financial difficulties. It’s always better to address potential issues before they become problems.

How to check your medical equipment loan payment status?

Checking your medical equipment loan payment status is essential to stay on top of your payments, avoid late fees, and ensure that your equipment continues functioning without interruption. Here are simple steps you can follow to track your payment status effectively:Review loan documents

When you first receive your medical equipment, review the loan agreement thoroughly. The agreement will contain essential details such as the total loan amount, payment schedule, due dates, and interest rates. This document is a good starting point to understand your financial obligations.

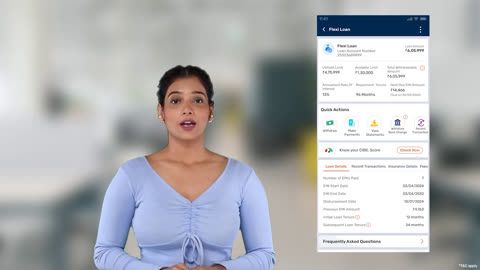

Visit the lender’s website or portal

Many lenders provide online platforms or mobile apps where you can log in and view your loan status. Once logged in, you can check the current balance, upcoming due dates, and previous payments. Ensure that your login credentials are secure for privacy reasons.

Set up payment reminders

Most lenders offer email or text alerts to remind you of upcoming payments. Set up these reminders to avoid missing deadlines. You can also configure notifications for any overdue payments or important changes to your loan terms.

Call the lender’s customer service

If you don’t have access to an online portal, or if you prefer speaking to someone directly, call your lender’s customer service line. Ask them for a current breakdown of your loan payment status, including the remaining balance, next due date, and any potential fees or penalties.

Check your bank statements

Cross-check your bank account or credit card statements to verify that payments have been deducted correctly. Ensure that no payments are missed or processed incorrectly. If there’s any discrepancy, reach out to your lender immediately for clarification.

Request an account statement

If you prefer a more formal overview of your payment status, request a written statement from your lender. This will provide a detailed history of payments made, outstanding amounts, and interest accrued. It can be useful for budgeting and ensuring everything is up to date.

Monitor payment history

Keeping track of your payment history will help you identify any potential issues, such as accidental missed payments or delayed transactions. A good payment history may also improve your credit score, especially if you’re paying on time.

Consider setting up automatic payments

To avoid forgetting payments, consider setting up automatic payments directly through your bank or lender. This can ensure that payments are made on time without you having to worry about manually making each payment.

Review loan status regularly

Make it a habit to review your loan status regularly, even when you’re not due for a payment. Monitoring your loan ensures there are no surprises and gives you peace of mind knowing exactly where you stand financially.

By following these simple steps, you can easily manage your medical equipment loan and ensure that your payments are on track. Consistent tracking and communication with your lender can help avoid any financial hiccups down the road.

Benefits of tracking your loan payment status

Tracking your loan payment status is a crucial habit that offers multiple advantages. Staying on top of your payments can improve your financial well-being and ensure that your medical equipment remains functional without interruption. Here are some key benefits of tracking your loan payment status:Avoid late fees and penalties

One of the most immediate benefits of tracking your loan payment status is preventing late fees and penalties. Missing a payment or paying late can result in additional charges, which can increase the overall cost of the loan. Regularly monitoring your payment status helps you stay on track and avoid unnecessary expenses.

Maintain good credit health

Timely payments play a significant role in maintaining or improving your credit score. Late or missed payments can negatively affect your credit rating, which could impact your ability to get approved for future loans or credit. By tracking your payments and ensuring they’re made on time, you safeguard your credit health.

Identify payment errors quickly

Regularly reviewing your loan payment status helps you spot discrepancies or errors in your account. For example, payments might be recorded incorrectly, or fees might be charged that shouldn’t be there. Early detection of such issues allows you to address them promptly with your lender.

Stay on top of loan terms

Loan agreements can have specific terms, such as fluctuating interest rates or the ability to make additional payments without penalties. By tracking your payment status, you stay informed about any changes in the loan's terms, such as updated due dates or interest rate adjustments. This helps you plan your budget accordingly and manage the loan more effectively.

Avoid service interruptions

When it comes to medical equipment, not paying on time can lead to interruptions in service, which could affect your ability to care for patients or manage your healthcare needs. By tracking your payment status, you ensure that payments are made on time and that your equipment continues to be available without disruption.

Budgeting and financial planning

Keeping track of your loan payment status allows you to factor your payments into your budget. By knowing how much is due and when, you can allocate funds accordingly, reducing the chances of financial strain. It helps you prioritise expenses and make adjustments if necessary to stay within your financial means.

Peace of mind

Regularly checking your loan status provides peace of mind. When you know your payments are up to date, and there are no surprises, you can focus on other aspects of life or work. Being proactive about your loan management reduces stress and provides confidence in your financial management.

Informed decision making

Tracking your payment status allows you to make informed decisions about refinancing, making extra payments, or exploring other options. If you’re ahead on payments, you may decide to pay off the loan faster, reducing the overall interest. Being aware of your loan status empowers you to take control of your financial future.

Improved financial relationships

Keeping up with loan payments strengthens your relationship with the lender. A consistent payment history reflects positively on you and may open up more favourable terms if you need future financial assistance. Lenders may be more inclined to offer discounts, better rates, or other benefits if you maintain a solid repayment record.

Common issues while checking loan payment status

Checking your loan payment status is a key step in managing your finances, but sometimes there are challenges that can arise during the process. Here are some common issues you may encounter while tracking your loan payment status and tips on how to resolve them:Incorrect loan balance displayed

Sometimes, the loan balance shown may be incorrect due to payment processing delays or data entry errors. This can happen if payments were made recently but haven’t been updated in the system yet.

Solution: Always check the date of the last payment and give it some time for the system to reflect changes. If the error persists, contact your lender for clarification and ask for an updated statement.

Technical issues with online portals

Online portals or mobile apps used to track your loan payment status may experience technical difficulties, such as login issues, slow loading times, or crashes.

Solution: Ensure that your internet connection is stable. If the problem is with the portal, try clearing your browser cache or updating the app. Contact customer support if the issue continues.

Delayed or missing payments

Sometimes, payments may be delayed or go missing in the system, making it appear as though you missed a payment. This can happen due to issues with bank transfers, processing errors, or misunderstandings about the payment method.

Solution: Double-check your bank statements or payment confirmation emails. If you find discrepancies, contact the lender to confirm whether the payment was received. Consider using automatic payments for smoother processing in the future.

Confusion over interest rates or fees

Some loan agreements may involve variable interest rates or additional fees that are hard to track. Confusion over how these are applied can make it difficult to understand your current payment status.

Solution: Review the loan agreement to understand how interest rates and fees are calculated. If there are any discrepancies, ask your lender for a breakdown of how your payments are being applied.

Difficulty navigating the loan management system

Some lenders use complicated or outdated systems for managing loans, which can make it difficult for borrowers to access accurate payment details quickly.

Solution: Reach out to customer support for guidance on how to navigate the system. You may also request that the lender provide statements via email or paper if the online system is difficult to use.

Disputes over payment dates

Loan agreements may include flexible payment dates, but confusion can arise about the exact due date. This is especially true when payments are made close to the end of the month or when the loan provider has set a specific day for payment each month.

Solution: Always verify your due dates and set calendar reminders ahead of time. If you miss a payment, ask for a grace period or clarification on due dates to avoid penalties.

Miscommunication or lack of updates

Sometimes, borrowers may not receive timely updates from their lenders, leaving them in the dark about the current status of their loan payments. This could lead to missed payments or misunderstandings about the loan’s progress.

Solution: Regularly check your account and ensure that the lender’s contact information is correct. Set up email or text alerts to receive updates on your payment status.

Unclear terms and conditions

In some cases, the terms and conditions related to your loan payments may not be clear, especially if the loan was taken out a long time ago. This can result in confusion about payment amounts, due dates, or loan details.

Solution: Review the loan agreement again or ask your lender for a detailed explanation of the terms. Understanding the specifics of your loan helps you avoid surprises down the line.

Security and privacy concerns

When checking your loan payment status online, there may be concerns about the security and privacy of your financial information. Data breaches or unsecured platforms can make it difficult to trust the loan management system.

Solution: Always ensure that the website or app you’re using is secure (look for HTTPS in the URL). Use strong, unique passwords, and enable two-factor authentication for additional protection.

Unforeseen changes in payment terms

In some cases, lenders may change the terms of the loan, such as interest rates or payment schedules, without clear communication. This can cause confusion about your payment status.

Solution: Read any communication from your lender thoroughly and immediately contact them if any changes are unclear. Ask for detailed explanations and request updated statements reflecting new terms.

Tips to ensure timely loan payments

Ensuring timely loan payments is essential to maintaining good financial health and avoiding unnecessary fees. Staying on top of your loan payment schedule can help you maintain a positive credit score and prevent service interruptions, especially when dealing with essential items like medical equipment. Here are some tips to help ensure timely loan payments:Set up automatic payments

One of the easiest ways to ensure your loan payments are made on time is to set up automatic payments. Link your bank account to your loan account, and have payments automatically deducted each month. This eliminates the risk of forgetting a payment. Pro Tip: If you want to track your payments, use your lender’s platform to check loan details regularly.

Use payment reminders

Set reminders on your phone or through your lender’s app or website. Most financial institutions allow you to receive payment alerts via email or SMS a few days before your due date. This gives you a heads-up to ensure the funds are available in your account.

Tip: Utilise your lender’s notification settings for reminders about your upcoming payments.

Review your loan payment schedule

Understanding when your payments are due and how much is required can help you prepare in advance. Regularly reviewing your loan payment schedule will allow you to allocate the necessary funds before the due date. Pro Tip: You can easily check loan details to keep track of the payment schedule.

Link your loan to your calendar

Synchronise your loan due dates with your digital calendar. Set recurring events or reminders for a few days before the payment is due. This visual aid can help you see upcoming payments alongside other financial obligations, helping you prioritise accordingly.

Maintain a separate savings account for loan payments

Having a separate account specifically for loan payments can prevent you from accidentally spending the money you’ve set aside for your loan. Deposit the required amount into this account every month, ensuring the funds are available when needed.

Plan for extra payments

If your loan allows it, consider making additional payments on your loan when you have extra funds. This can reduce your balance and shorten the repayment period, but it also helps keep you ahead in case of unexpected events that might affect your finances.

Check your loan statement regularly

Regularly reviewing your loan statements will help you stay informed about your balance, interest rates, and upcoming payment amounts. This will give you enough time to plan for payments or adjust your budget accordingly. Tip: You can view your Bajaj EMI loan statement to see detailed information about your loan payments and history.

Ensure sufficient funds are available

Before the payment date, ensure that your account has sufficient funds to cover the loan payment. Insufficient funds can result in failed payments and possible fees. Keep track of your account balances to avoid this issue.

Review and adjust your budget

Make sure your loan payment is factored into your monthly budget. Track your spending habits and make adjustments as needed to prioritise loan repayments. This can help you avoid any financial strain when payment time comes.

Communicate with your lender in case of difficulty

If you’re facing financial hardship or foresee difficulty in making a payment on time, contact your lender immediately. Many lenders offer payment deferrals or flexible plans in case of financial difficulties. It’s always better to address potential issues before they become problems.