3 min

10-April-2025

Managing your finances smartly is all about flexibility — and that’s exactly what Part Prepay for Loan Against Securities offers. This facility empowers borrowers to reduce their outstanding loan amount by making partial prepayments at their convenience, without disturbing their investment portfolio. Whether you’ve pledged shares, mutual funds, bonds, or other eligible securities, Part Prepay allows you to lower your interest burden and shorten your repayment tenure, giving you greater control over your loan lifecycle. Unlike full prepayment, this option lets you pay off portions of your loan as and when you have surplus funds, helping you manage cash flow efficiently. Plus, many lenders offer this facility with minimal or no prepayment charges, making it a cost-effective strategy to manage your liabilities. By opting for Part Prepay, you not only safeguard your investments but also enjoy the dual benefit of liquidity and reduced debt stress — a win-win for smart borrowers.

Unlike full prepayment, where you clear the entire outstanding balance, part-prepayment enables you to pay off smaller amounts whenever you have surplus funds. This proactive approach helps reduce the principal amount, which directly lowers your future interest payments, as interest is typically charged only on the outstanding balance. Moreover, part-prepayment can help shorten the loan tenure, ease your financial burden, and improve your overall cash flow management.

Most lenders today allow part-prepayment on loans against securities with little to no additional charges, making it an attractive option for borrowers looking to optimize their repayment strategy. It’s particularly useful in scenarios where you might receive irregular inflows of cash, such as bonuses, investment returns, or freelance income, allowing you to make payments without waiting to accumulate the full amount for complete closure.

By choosing part-prepayment, you maintain ownership of your pledged securities, continue to enjoy potential capital appreciation or dividends, and reduce your debt progressively. This option strikes the perfect balance between liquidity and debt management, making it a smart financial move for borrowers who want to stay in control of their obligations without liquidating their investments.

Reduction in interest burden

By part-prepaying, you lower your outstanding principal amount. Since interest is calculated on the reduced balance, you end up paying less interest over the remaining loan tenure, resulting in significant savings.

Shorter loan tenure

Regular part-prepayments can help you close your loan much earlier than the original term. This reduces your overall debt cycle and frees up future income for other financial goals.

Improved cash flow management

Part-prepayment gives you flexibility. You can make payments whenever you have surplus funds, such as bonuses, tax refunds, or investment returns, without waiting for large lump sums.

No need to liquidate investments

One of the biggest advantages of LAS is that you retain ownership of your securities. With part-prepayment, you reduce your loan burden without selling your investments, allowing them to continue appreciating or generating returns.

Minimal or zero prepayment charges

Many lenders offer part-prepayment options with little to no penalties. This cost-effective feature encourages borrowers to repay early without worrying about extra fees.

Boosts creditworthiness

Timely part-prepayments reflect positively on your credit profile. It showcases disciplined repayment behaviour, which can enhance your credit score and improve eligibility for future loans.

Flexible repayment strategy

Part-prepayment is entirely at your discretion. Whether you want to pay small amounts monthly or larger sums periodically, you have complete control over how you manage your repayments.

Peace of mind

Reducing your outstanding balance progressively relieves financial stress. It provides psychological comfort, knowing you’re steadily lowering your liabilities.

Maintains investment growth potential

Since your pledged securities remain invested, they continue to benefit from market growth, dividends, or interest, ensuring your wealth-building journey stays on track.

Readiness for emergencies

With reduced loan liability, you can unlock higher drawing power from your securities in the future if required, providing an emergency financial cushion.

Active loan account

You must have an active and running Loan Against Securities account with the lender. Part-prepayment is applicable only to existing loan accounts, not during the loan application stage.

Minimum prepayment amount

Lenders often specify a minimum amount for part-prepayment. Ensure that the amount you intend to pay meets or exceeds this threshold to process the payment successfully.

No outstanding dues or penal charges

Borrowers should ensure that there are no pending dues, penalties, or unpaid charges on their loan account. Some lenders require accounts to be in good standing to accept part-prepayments.

Eligible securities as collateral

The securities pledged against the loan must continue to remain eligible as per the lender’s policies. If the value of the pledged securities drops significantly or they become ineligible, part-prepayment options may be restricted.

Compliance with lender's terms and conditions

The loan agreement should permit part-prepayments. Review your loan documents to confirm whether part-prepayment is allowed and under what conditions.

Prepayment timing restrictions (if any)

Some lenders may specify a waiting period or restrict part-prepayments during certain phases of the loan, such as the initial months. Check for any such timing clauses in your agreement.

Borrower identity verification

To process part-prepayment, the borrower may need to verify their identity or authenticate the transaction through secure channels, especially for online payments.

Adequate funds in linked account

If you’re making the part-prepayment via an auto-debit or online transfer, ensure that your bank account linked to the loan has sufficient funds to cover the payment.

Prepayment request submission

Some lenders require an official request or online submission before accepting part-prepayment. Confirm the process and documentation requirements in advance.

Adherence to regulatory guidelines

All part-prepayments must comply with applicable banking and regulatory norms, as prescribed by financial authorities.

Step 1: Review your loan agreement

Begin by carefully reading your loan documents to understand the terms related to part-prepayment, including any minimum amount requirements, charges, or restrictions.

Step 2: Check outstanding loan balance

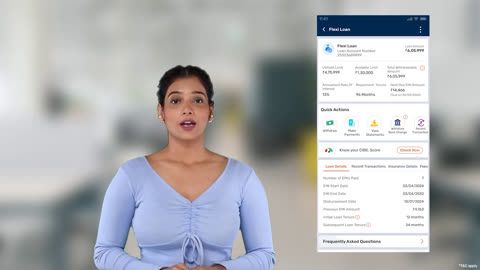

Log in to your loan account through the lender’s online portal or contact customer support to confirm your current outstanding principal and accrued interest.

Step 3: Ensure sufficient funds

Make sure you have enough funds available in your bank account or the payment source from which you intend to make the part-prepayment.

Step 4: Initiate prepayment request

Some lenders require you to submit a prepayment request through their digital platform, mobile app, or by visiting a branch. Follow the prescribed method.

Step 5: Select payment mode

Choose a convenient payment mode such as net banking, debit card, UPI, NEFT, or cheque deposit, depending on the lender’s accepted options.

Step 6: Confirm transaction details

Double-check the prepayment amount, loan account number, and payment mode before proceeding to avoid any errors.

Step 7: Complete the payment

Authorise the transaction and complete the payment process. Keep the transaction confirmation or receipt for your records.

Step 8: Obtain acknowledgement from lender

After the payment is processed, request an official acknowledgment or updated loan statement reflecting the part-prepayment.

Step 9: Monitor loan account

Regularly check your loan account to ensure the prepayment has been correctly applied and track the reduced outstanding balance.

Online payment via net banking

Most lenders provide a secure online portal where you can log in and make direct payments through net banking. This method is quick, safe, and allows you to track your transactions instantly.

Mobile banking app

Use your lender’s mobile application to initiate part-prepayments. Mobile apps are user-friendly and allow you to pay anytime, anywhere, with a few taps on your smartphone.

UPI (Unified Payments Interface)

UPI is a fast and convenient option. Simply use your UPI-enabled app to transfer the part-prepayment amount directly to your loan account using the lender’s UPI ID or QR code.

NEFT/RTGS transfer

You can make payments through NEFT (National Electronic Funds Transfer) or RTGS (Real-Time Gross Settlement) from your bank account to the lender’s designated account. Ensure you enter accurate loan account details while making the transfer.

Auto-debit facility

Some lenders allow you to set up an auto-debit mandate. You can instruct your bank to automatically debit a specific amount from your account towards part-prepayment on scheduled dates.

Cheque or demand draft submission

Traditional methods like issuing a cheque or demand draft in favour of your lender are still accepted by many institutions. Submit it at the nearest branch along with your loan account details.

In-person payment at bank branch

Visit your lender’s branch and make the payment over the counter. The bank staff will assist you in processing the part-prepayment and provide a receipt for your records.

Customer service assistance

Contact your lender’s customer care or relationship manager for guided assistance. They can help you understand available payment modes and assist in completing the transaction.

Payment through loan statement link

Some lenders send monthly loan statements with embedded payment links. You can use these links to make part-prepayments quickly and securely.

Third-party payment platforms (if allowed)

Select lenders may partner with trusted third-party platforms for easier loan repayments. Always verify the platform's authenticity before proceeding.

Reduces outstanding principal amount

Part-prepayments directly lower your principal balance. A reduced principal means the interest charged on your loan also decreases, leading to overall cost savings.

Lowers your EMI (if opted for)

After a part-prepayment, you may choose to reduce your EMI amount. This is beneficial if you wish to ease your monthly financial burden while continuing the loan as planned.

Shortens loan tenure (if opted for)

Alternatively, you can maintain the same EMI amount and reduce your loan tenure instead. This helps you repay your loan faster and save on total interest outgo.

Flexible repayment strategy

Part-prepayment gives you the flexibility to choose between lowering EMIs or shortening the tenure, depending on your financial goals and cash flow preferences.

Fewer EMIs, lower interest cost

Opting to shorten your loan tenure means fewer EMIs, which significantly reduces the total interest paid over the life of the loan.

Better loan management With reduced outstanding balance, it becomes easier to track and manage your repayments. Always refer to your loan account number for accurate tracking and transactions.

Enhanced credit profile

Timely part-prepayments reflect responsible credit behaviour, which can boost your credit score and make future borrowings easier.

Step towards complete repayment Part-prepayment is an effective strategy to work towards full loan closure. To understand more, explore how to repay loan efficiently.

What is part-prepayment for a loan against securities?

Part-prepayment for a Loan Against Securities (LAS) refers to the option of repaying a portion of your outstanding loan balance before the scheduled repayment date. When you take a loan against securities, such as shares, mutual funds, bonds, or other marketable investments, you pledge these assets as collateral to secure the loan. While the primary benefit of LAS is maintaining your investments while accessing funds, part-prepayment adds further flexibility by allowing you to gradually reduce your loan liability over time.Unlike full prepayment, where you clear the entire outstanding balance, part-prepayment enables you to pay off smaller amounts whenever you have surplus funds. This proactive approach helps reduce the principal amount, which directly lowers your future interest payments, as interest is typically charged only on the outstanding balance. Moreover, part-prepayment can help shorten the loan tenure, ease your financial burden, and improve your overall cash flow management.

Most lenders today allow part-prepayment on loans against securities with little to no additional charges, making it an attractive option for borrowers looking to optimize their repayment strategy. It’s particularly useful in scenarios where you might receive irregular inflows of cash, such as bonuses, investment returns, or freelance income, allowing you to make payments without waiting to accumulate the full amount for complete closure.

By choosing part-prepayment, you maintain ownership of your pledged securities, continue to enjoy potential capital appreciation or dividends, and reduce your debt progressively. This option strikes the perfect balance between liquidity and debt management, making it a smart financial move for borrowers who want to stay in control of their obligations without liquidating their investments.

Benefits of part-prepaying your loan against securities

Part-prepaying your Loan Against Securities (LAS) is a strategic way to manage your debt while keeping your investments intact. Here’s how it benefits you:Reduction in interest burden

By part-prepaying, you lower your outstanding principal amount. Since interest is calculated on the reduced balance, you end up paying less interest over the remaining loan tenure, resulting in significant savings.

Shorter loan tenure

Regular part-prepayments can help you close your loan much earlier than the original term. This reduces your overall debt cycle and frees up future income for other financial goals.

Improved cash flow management

Part-prepayment gives you flexibility. You can make payments whenever you have surplus funds, such as bonuses, tax refunds, or investment returns, without waiting for large lump sums.

No need to liquidate investments

One of the biggest advantages of LAS is that you retain ownership of your securities. With part-prepayment, you reduce your loan burden without selling your investments, allowing them to continue appreciating or generating returns.

Minimal or zero prepayment charges

Many lenders offer part-prepayment options with little to no penalties. This cost-effective feature encourages borrowers to repay early without worrying about extra fees.

Boosts creditworthiness

Timely part-prepayments reflect positively on your credit profile. It showcases disciplined repayment behaviour, which can enhance your credit score and improve eligibility for future loans.

Flexible repayment strategy

Part-prepayment is entirely at your discretion. Whether you want to pay small amounts monthly or larger sums periodically, you have complete control over how you manage your repayments.

Peace of mind

Reducing your outstanding balance progressively relieves financial stress. It provides psychological comfort, knowing you’re steadily lowering your liabilities.

Maintains investment growth potential

Since your pledged securities remain invested, they continue to benefit from market growth, dividends, or interest, ensuring your wealth-building journey stays on track.

Readiness for emergencies

With reduced loan liability, you can unlock higher drawing power from your securities in the future if required, providing an emergency financial cushion.

Eligibility criteria for part-prepayment of loan against securities

Before opting for part-prepayment of your Loan Against Securities (LAS), it’s essential to understand the eligibility criteria set by lenders. While these may vary slightly from one institution to another, the following are the common requirements you should be aware of:Active loan account

You must have an active and running Loan Against Securities account with the lender. Part-prepayment is applicable only to existing loan accounts, not during the loan application stage.

Minimum prepayment amount

Lenders often specify a minimum amount for part-prepayment. Ensure that the amount you intend to pay meets or exceeds this threshold to process the payment successfully.

No outstanding dues or penal charges

Borrowers should ensure that there are no pending dues, penalties, or unpaid charges on their loan account. Some lenders require accounts to be in good standing to accept part-prepayments.

Eligible securities as collateral

The securities pledged against the loan must continue to remain eligible as per the lender’s policies. If the value of the pledged securities drops significantly or they become ineligible, part-prepayment options may be restricted.

Compliance with lender's terms and conditions

The loan agreement should permit part-prepayments. Review your loan documents to confirm whether part-prepayment is allowed and under what conditions.

Prepayment timing restrictions (if any)

Some lenders may specify a waiting period or restrict part-prepayments during certain phases of the loan, such as the initial months. Check for any such timing clauses in your agreement.

Borrower identity verification

To process part-prepayment, the borrower may need to verify their identity or authenticate the transaction through secure channels, especially for online payments.

Adequate funds in linked account

If you’re making the part-prepayment via an auto-debit or online transfer, ensure that your bank account linked to the loan has sufficient funds to cover the payment.

Prepayment request submission

Some lenders require an official request or online submission before accepting part-prepayment. Confirm the process and documentation requirements in advance.

Adherence to regulatory guidelines

All part-prepayments must comply with applicable banking and regulatory norms, as prescribed by financial authorities.

Step-by-step guide on how to part-prepay your loan against securities

Part-prepaying your Loan Against Securities (LAS) is a simple and efficient process. Here’s a step-by-step guide to help you navigate it smoothly:Step 1: Review your loan agreement

Begin by carefully reading your loan documents to understand the terms related to part-prepayment, including any minimum amount requirements, charges, or restrictions.

Step 2: Check outstanding loan balance

Log in to your loan account through the lender’s online portal or contact customer support to confirm your current outstanding principal and accrued interest.

Step 3: Ensure sufficient funds

Make sure you have enough funds available in your bank account or the payment source from which you intend to make the part-prepayment.

Step 4: Initiate prepayment request

Some lenders require you to submit a prepayment request through their digital platform, mobile app, or by visiting a branch. Follow the prescribed method.

Step 5: Select payment mode

Choose a convenient payment mode such as net banking, debit card, UPI, NEFT, or cheque deposit, depending on the lender’s accepted options.

Step 6: Confirm transaction details

Double-check the prepayment amount, loan account number, and payment mode before proceeding to avoid any errors.

Step 7: Complete the payment

Authorise the transaction and complete the payment process. Keep the transaction confirmation or receipt for your records.

Step 8: Obtain acknowledgement from lender

After the payment is processed, request an official acknowledgment or updated loan statement reflecting the part-prepayment.

Step 9: Monitor loan account

Regularly check your loan account to ensure the prepayment has been correctly applied and track the reduced outstanding balance.

Methods to make a part-prepayment on your loan against securities

Lenders offer multiple convenient methods to make a part-prepayment on your Loan Against Securities (LAS). You can choose the option that best suits your preferences and financial planning. Here’s a list of common methods:Online payment via net banking

Most lenders provide a secure online portal where you can log in and make direct payments through net banking. This method is quick, safe, and allows you to track your transactions instantly.

Mobile banking app

Use your lender’s mobile application to initiate part-prepayments. Mobile apps are user-friendly and allow you to pay anytime, anywhere, with a few taps on your smartphone.

UPI (Unified Payments Interface)

UPI is a fast and convenient option. Simply use your UPI-enabled app to transfer the part-prepayment amount directly to your loan account using the lender’s UPI ID or QR code.

NEFT/RTGS transfer

You can make payments through NEFT (National Electronic Funds Transfer) or RTGS (Real-Time Gross Settlement) from your bank account to the lender’s designated account. Ensure you enter accurate loan account details while making the transfer.

Auto-debit facility

Some lenders allow you to set up an auto-debit mandate. You can instruct your bank to automatically debit a specific amount from your account towards part-prepayment on scheduled dates.

Cheque or demand draft submission

Traditional methods like issuing a cheque or demand draft in favour of your lender are still accepted by many institutions. Submit it at the nearest branch along with your loan account details.

In-person payment at bank branch

Visit your lender’s branch and make the payment over the counter. The bank staff will assist you in processing the part-prepayment and provide a receipt for your records.

Customer service assistance

Contact your lender’s customer care or relationship manager for guided assistance. They can help you understand available payment modes and assist in completing the transaction.

Payment through loan statement link

Some lenders send monthly loan statements with embedded payment links. You can use these links to make part-prepayments quickly and securely.

Third-party payment platforms (if allowed)

Select lenders may partner with trusted third-party platforms for easier loan repayments. Always verify the platform's authenticity before proceeding.

How part-prepayment affects your loan against securities EMI and tenure?

Making a part-prepayment towards your Loan Against Securities (LAS) can have a positive impact on both your EMI and loan tenure. Here’s how:Reduces outstanding principal amount

Part-prepayments directly lower your principal balance. A reduced principal means the interest charged on your loan also decreases, leading to overall cost savings.

Lowers your EMI (if opted for)

After a part-prepayment, you may choose to reduce your EMI amount. This is beneficial if you wish to ease your monthly financial burden while continuing the loan as planned.

Shortens loan tenure (if opted for)

Alternatively, you can maintain the same EMI amount and reduce your loan tenure instead. This helps you repay your loan faster and save on total interest outgo.

Flexible repayment strategy

Part-prepayment gives you the flexibility to choose between lowering EMIs or shortening the tenure, depending on your financial goals and cash flow preferences.

Fewer EMIs, lower interest cost

Opting to shorten your loan tenure means fewer EMIs, which significantly reduces the total interest paid over the life of the loan.

Better loan management With reduced outstanding balance, it becomes easier to track and manage your repayments. Always refer to your loan account number for accurate tracking and transactions.

Enhanced credit profile

Timely part-prepayments reflect responsible credit behaviour, which can boost your credit score and make future borrowings easier.

Step towards complete repayment Part-prepayment is an effective strategy to work towards full loan closure. To understand more, explore how to repay loan efficiently.