Repaying a Chartered Accountant (CA) Loan efficiently is vital for maintaining financial stability and ensuring continued access to professional credit. CA loan repayment schedule outlines the timeline and structure of EMIs (Equated Monthly Instalments), providing a clear roadmap to help borrowers manage their dues over the loan tenure. This schedule includes details such as due dates, interest amounts, principal breakdowns, and total outstanding balance over time. For professionals juggling client commitments and practice growth, a well-organised repayment plan simplifies debt management and helps avoid defaults.

An accurate understanding of your EMI amount, interest rate, tenure, and flexibility in repayment is crucial to avoid financial strain. Moreover, being proactive in addressing missed payments, restructuring your repayment terms, or clearing dues online can protect your credit score and reduce stress. This guide explores EMI calculation, scheduling methods, common pitfalls, and how to optimise your CA loan repayment strategy. Whether you are just starting repayment or seeking to revise your plan, this resource ensures clarity and control.

How is the CA loan EMI calculated?

The Equated Monthly Instalment (EMI) for a Chartered Accountant (CA) loan is calculated using a specific financial formula that accounts for the loan amount, interest rate, and tenure. EMI is the fixed amount you pay every month towards the repayment of your loan, and it includes both the principal and interest components. The formula used is:

EMI = [P × R × (1+R)^N] / [(1+R)^N – 1]

Where:

P is the principal amount or loan amount.

R is the monthly interest rate, which is the annual rate divided by 12 and expressed as a decimal.

N is the loan tenure in months.

For example, if you borrow ₹5,00,000 at an annual interest rate of 12% for 3 years (36 months), your monthly interest rate would be 1% or 0.01. Substituting the values into the formula gives you the EMI.

Using the formula: EMI = [500000 × 0.01 × (1+0.01)^36] / [(1+0.01)^36 – 1]

This gives an approximate EMI of ₹16,607.

Over the tenure, the EMI remains constant in case of a fixed interest rate. However, the interest and principal portions of each instalment vary. Early instalments primarily go towards paying off interest, while later instalments cover more of the principal.

Most lenders provide an amortisation schedule, which is a detailed table showing how each EMI is split between interest and principal across the tenure. It also shows the outstanding balance after every instalment. This helps borrowers keep track of repayment and understand how their loan is progressing.

Borrowers can also use free online EMI calculators, which require inputting loan amount, interest rate, and tenure. These tools instantly display the EMI, total interest payable, and total repayment amount, offering clarity for budgeting.

Understanding how the EMI is calculated helps borrowers plan better and avoid over-borrowing. It also ensures transparency in the repayment process and supports long-term financial discipline.

Steps to create a repayment schedule for CA loan

Creating a repayment schedule for a Chartered Accountant (CA) loan is essential to ensure timely repayments, financial discipline, and better cash flow management. A well-planned schedule helps you visualise your monthly obligations and prepares you for potential changes during the loan tenure. Here are step-by-step pointers to help you build a robust CA loan repayment schedule:

- Review your loan agreement thoroughlyStart by understanding your loan's key details: sanctioned amount, interest rate (fixed or floating), EMI amount, tenure, disbursement date, and applicable charges.

- Use an EMI calculatorCalculate your monthly EMI using an online loan EMI calculator by entering the loan amount, interest rate, and tenure. This will help you estimate your total repayment burden.

- Obtain the amortisation schedule from your lenderThis schedule outlines each EMI’s breakdown, showing the interest and principal components, as well as the outstanding balance after every payment.

- Set monthly EMI due date remindersUse mobile calendar alerts, reminders, or banking apps to notify you a few days before your EMI due date. Consistent reminders help avoid delays.

- Automate your EMI paymentsOpt for auto-debit facilities through your bank account to ensure timely EMI payments without manual intervention each month.

- Allocate a monthly budget for EMIsAdjust your budget to prioritise EMI payments. Set aside the EMI amount at the beginning of each month to prevent last-minute cash shortages.

- Build an emergency buffer fundSet aside savings equivalent to at least 2–3 months of EMIs. This buffer provides safety during unforeseen events like delayed payments, job loss, or emergencies.

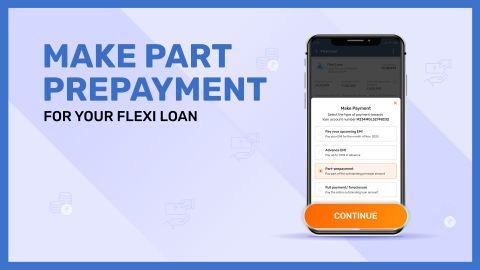

- Account for additional income or bonusesWhen you receive extra income, consider using it to make part-prepayments to reduce your outstanding principal and interest burden.

- Monitor your bank account regularlyCheck for EMI deductions and ensure there are no failed transactions. Also, reconcile your repayment progress with your amortisation table.

- Plan for early repayment optionsIf your financial condition improves, consider making lump sum payments to reduce the loan tenure or EMI burden. Check for any prepayment charges.

- Record and store your repayment historyMaintain a digital or physical record of EMI payments, including bank transaction details, receipts, and emails from the lender for future reference.

- Update your repayment schedule when neededLife circumstances may change. Update your repayment plan accordingly if you refinance, restructure the loan, or receive a moratorium.

- Keep track of your NOC statusAfter the loan is fully paid off, request and retain a No Objection Certificate (NOC) from the lender to close your loan account officially.

Following these steps ensures you remain in control of your CA loan, avoid penalties, and maintain a positive credit history throughout the repayment journey.

Benefits of following a structured repayment plan

- Improves your credit scoreTimely EMI payments reflect positively on your credit report. A consistent repayment record boosts your creditworthiness, increasing your eligibility for future loans or credit facilities at better interest rates.

- Reduces overall interest burdenSticking to your repayment schedule avoids missed payments and delays. Regular payments can also enable you to make prepayments, thereby reducing the principal and saving on total interest payable.

- Helps with financial planningWith a fixed EMI and tenure, you can plan your monthly and yearly budgets accurately. Knowing your exact financial obligation allows you to allocate income effectively for savings, expenses, and investments.

- Prevents late fees and penaltiesA structured plan ensures on-time payments, eliminating late charges and other penalties that increase your loan’s total cost and add unnecessary financial stress.

- Provides clarity on outstanding duesA structured repayment plan supported by an amortisation schedule helps you clearly track how much you have repaid and how much is still pending. This aids in monitoring financial progress.

- Supports early loan closureWith disciplined repayments and occasional part-prepayments, you may be able to close your loan before the scheduled end date. Early closure helps in saving interest and improves cash flow.

- Strengthens lender trustFollowing a repayment plan improves your relationship with the lender. Trustworthy borrowers often receive quicker approvals for top-up loans, balance transfers, or future financial products.

- Helps avoid legal or default issuesAdhering to the plan protects you from default notices or legal actions that arise from missed or bounced EMIs.

- Encourages financial disciplineRepaying a loan consistently instils a sense of accountability and builds habits that are beneficial for long-term financial management.

- Creates an emergency buffer mindsetIndividuals with structured plans often maintain emergency funds to avoid EMI defaults, which adds a layer of financial security during unexpected events.

- Improves long-term credit accessA well-maintained repayment history makes it easier to access bigger loans like home loans or business loans when needed.

- Reduces financial anxietyA structured plan eliminates guesswork. With fixed dates and amounts, you can mentally and financially prepare each month, reducing uncertainty and stress.

- Enables smarter cash flow managementWith predictable outflows, you can align your spending patterns and income to optimise liquidity and avoid crunch periods.

By following a structured repayment plan, you maintain financial control, minimise risks, and set yourself up for long-term stability and borrowing success.

Common mistakes to avoid in CA loan repayment

- Missing EMI deadlinesDelayed EMI payments can lead to late fees, increased interest, and a drop in your credit score. Consistent delays can severely affect your financial credibility.

- Not setting up auto-debit or remindersForgetting payment dates is common. Failing to automate payments or set reminders may result in accidental defaults that damage your repayment history.

- Overlooking prepayment opportunitiesIgnoring chances to make part-prepayments wastes the opportunity to reduce your loan’s interest burden and shorten the repayment period.

- Not reviewing the repayment scheduleFailing to periodically check your amortisation schedule may lead to missed rate changes or miscalculations in your repayment progress.

- Using credit cards for EMI paymentsPaying EMIs through credit cards can attract high interest if the card balance is not repaid in full, adding to your financial stress.

- Ignoring changes in interest ratesWith floating rate loans, not tracking interest rate fluctuations can cause your EMIs to increase without you realising. Stay informed and adjust accordingly.

- Skipping documentationNot storing payment proofs or lender communications can cause issues during foreclosure or disputes. Always maintain a digital or physical record of transactions.

- Not checking NOC status after full repaymentAfter repaying the full loan amount, failing to collect and confirm the NOC may leave your loan record active in credit bureau reports.

- Delaying communication with the lenderIf you are struggling to make payments, not informing your lender in time may result in penalties or missed restructuring opportunities.

- Borrowing without proper repayment planningTaking a loan without assessing your monthly obligations, income flow, or emergency reserves may lead to financial strain and potential default.

Avoiding these mistakes can help ensure smoother loan management, protect your credit health, and allow for more financial flexibility throughout the loan tenure.

How to adjust your CA loan repayment schedule

- Review your current repayment terms. Begin by assessing your existing loan agreement. Understand the EMI amount, interest rate, tenure, and any prepayment or restructuring clauses mentioned in your loan documents.

- Contact your lender for available options. Speak to your loan provider to explore flexible repayment options. Most lenders offer restructuring or adjustment facilities depending on your repayment history and current financial situation.

- Request an extension in loan tenure. If your monthly EMI is too high, ask the lender to increase the loan tenure. This lowers the EMI amount, making it easier to manage, though it may increase total interest payable.

- Consider part-prepayment to reduce EMI or tenure. If you receive surplus income or bonuses, make a part-prepayment towards the loan. It can help reduce the outstanding principal, lowering either the EMI or the loan duration.

- Opt for balance transfer to another lender. If your current interest rate is high, switching to another lender offering better terms can help reduce your EMI or total repayment burden.

- Align EMI dates with income cycles. Adjust your EMI payment date to match your salary or primary income credit date. This helps avoid missed payments due to cash flow mismatches.

- Monitor interest rate changes regularly. For floating rate loans, keep track of market rate fluctuations. If the rate decreases, you might be eligible for revised EMIs or tenure adjustments upon request.

- Consolidate multiple loans if needed. If you have more than one loan, consider consolidating them into a single loan with a more manageable EMI structure and potentially lower interest rates.

- Use overdue online payment options if you’ve missed EMIs. If you have already fallen behind on your EMIs, clear them using the official online portal and reset your repayment schedule immediately.

- Update your financial plan accordingly. Once adjustments are made, revise your monthly budget and repayment calendar. This ensures you accommodate the new EMI structure without compromising essential expenses.

- Keep track of your updated amortisation schedule. Ask your lender for a revised amortisation table. It will help you visualise the remaining tenure, updated EMIs, and outstanding principal over time.

Adjusting your CA loan repayment schedule is a proactive step to maintain financial stability. By acting early and staying informed, you can manage your loan responsibly without risking defaults.

Conclusion

Managing your CA loan efficiently begins with understanding how EMI is calculated and planning a structured repayment schedule. A well-thought-out plan not only ensures financial stability but also protects your credit health and strengthens your relationship with lenders. Avoiding common repayment mistakes, tracking your NOC status, and using available options like overdue online payment.

Loan support made easy

| Wrong Linking Account for Ca Loan Emi Deduction |